Summary

- What a difference a month can make. Discussions have pivoted from interest rate cuts in the US to the possibility of an increase, while Chinese equities have rallied sharply on a combination of attractive value and hopes of effective policy implementation.

- The Chinese government’s efforts to address the country’s property market woes sparked a renewed and much-awaited rally in the Chinese equity markets. Even though demand for real estate remains weak in China, the government appears committed to completing the delivery of residential properties that were paid for. Elsewhere, we continue to favour India, and ASEAN is still attractive despite recent currency headwinds.

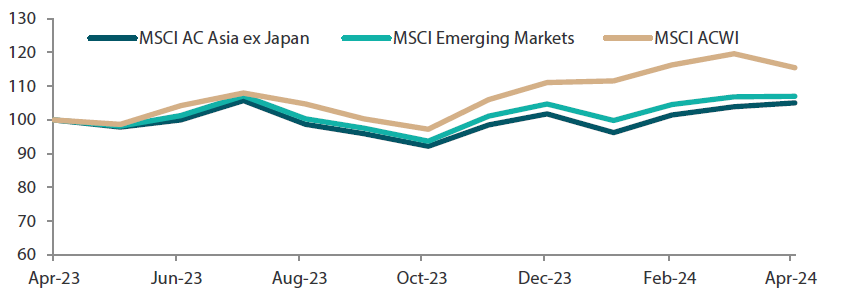

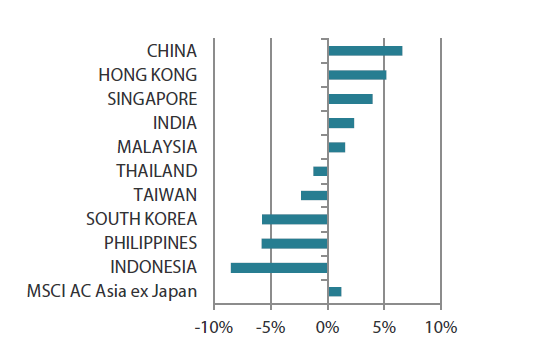

- In April, the MSCI AC Asia ex Japan Index climbed 1.2% in US dollar (USD) terms. China (+6.6%) and Hong Kong (+5.2%) led the region, while Indonesia (-8.5%) and the Philippines (-5.8%) were the laggards. The global equity rally at the start of the year came to a halt in April, as a string of hotter-than-expected inflation data in the US gave rise to worries that the US Federal Reserve (Fed) will not ease monetary policy as quickly as previously hoped.

- Investors are now recalibrating their interest rate outlook, marking a shift from the start of the year when the Fed was expected to cut rates as many as seven times in 2024. Asian central banks are feeling the pressure to shore up their currencies, and Indonesia’s central bank moved first by delivering a surprise rate hike. Ultimately, inflation remains a challenge. Previously, North Asia was expected to benefit from the surge in demand for artificial intelligence (AI). However, the market is now taking a more cautious approach and it has started to reward value instead of growth. We are currently in a period of changing expectations.

Market review

Asian markets outperform as global equities mostly pull back

The global equity rally that marked the start of the year has been overshadowed by concerns that central banks, especially the Fed, will not ease monetary policy as quickly as previously hoped due to sticky inflation, in addition to heightened geopolitical risks. The US dollar was markedly higher against most Asian currencies, but Asian equities still ended the month as clear outperformers thanks to China’s strong performance. The MSCI Asia Ex Japan Index gained 1.2% in USD terms in April.

Chart 1: 1-yr market performance of MSCI AC Asia ex Japan vs. Emerging Markets vs. All Country World Index

Source: Bloomberg, 30 April 2024. Returns are in USD. Past performance is not necessarily indicative of future performance.

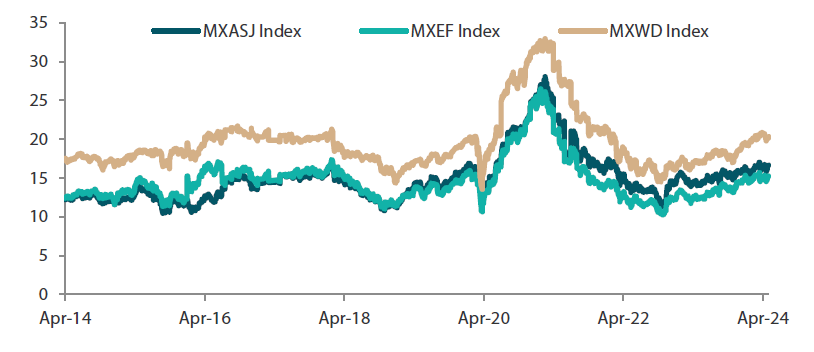

Chart 2: MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index price-to-earnings

Source: Bloomberg, 30 April 2024. Returns are in USD. Past performance is not necessarily indicative of future performance.

Chinese stocks standout performers amid growth hopes

Chinese stocks rose 6.6%, driven by a series of supportive measures aimed to promote the “high-quality” development of China’s capital market. The evaluation criteria for companies seeking to list in China will be enhanced, which will include a requirement for companies to disclose their dividend policies. Chinese authorities will also strengthen their supervision of listed companies. In economic news, China’s first-quarter economic growth was stronger than expected, driven mainly by robust growth in high-tech manufacturing. The country’s Q1 gross domestic product grew by 5.3% year-on-year (YoY) and 1.6% quarter-on-quarter (QoQ). The rise in China’s consumer price index slowed to 0.1% YoY in March, edging back towards zero. Hong Kong stocks (+5.2%) rebounded after a weak start to the year. The rebound came after China’s market regulator announced that it will facilitate the listings of Chinese companies in Hong Kong and expand the Stock Connect cross-border investment scheme to boost the city’s status as an international financial centre.

In South Korea (-5.8%), the central bank kept its key policy rate at 3.5%, a level it characterised as restrictive, suggesting that it might be difficult to reduce rates this year. South Korea's GDP growth accelerated in the first quarter of 2024 (+1.3% QoQ and +3.4% YoY), boosted by increased construction activity and higher private spending. Taiwan (-2.3%) saw its economy expand 6.5% YoY during the first quarter of 2024, benefitting from an increase in global demand for hardware underpinning AI technologies. Correspondingly, Taiwan’s exports jumped 18.9% in March, the fastest pace in two years. Index heavyweight TSMC beat revenue and profit expectations in the first quarter, buoyed by continued strong demand for advanced chips.

Central banks in ASEAN grapple with currency pressure

In ASEAN, central banks are bracing for more turbulence stemming from a stronger US dollar, and policymakers emphasised the stability of their respective currencies over the month. In the Philippines (-5.8%), Bangko Sentral ng Pilipinas kept its key interest rate at 6.5%. However, the central bank sounded more hawkish, ruling out rate cuts before the third quarter. In Thailand (-1.3%), the country’s central bank held its benchmark rate steady at 2.5%, citing ongoing worries over household debt and views that monetary policy would have limited effect on resolving structural economic problems. Meanwhile, in Indonesia (-8.5%), the central bank defied broad projections that it would stand pat and lifted its benchmark interest rate by 25 basis points to 6.25%, emphasising the need to stabilise the Indonesian rupiah against deteriorating global risks. Singapore (+4.0%) was the standout performer during the month as the Monetary Authority of Singapore kept its exchange rate-based monetary policy unchanged. Policy continuity is also expected; on 15 May, Singapore welcomed a new prime minister who succeeded Lee Hsien Loong.

Indian equities continue to exhibit robust growth

Indian equities (+2.3%) found support from the strong performance of the banking and auto sectors, fuelled by impressive March quarter earnings. The Reserve Bank of India (RBI)’s monetary policy committee kept its key lending rate unchanged at 6.5%, while India's annual retail inflation rate eased in March to a five-month low of 4.85% YoY. Voting for India’s general election has started and will continue over the next six weeks, in seven phases, until 1 June. Prime Minister Narendra Modi and his Bharatiya Janata Party are widely expected to win a third term in office.

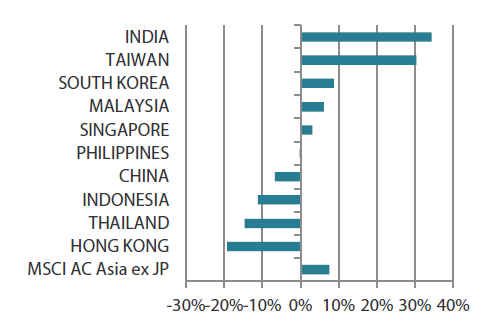

Chart 3: MSCI AC Asia ex Japan Index1

|

For the month ending 30 April 2024

|

For the year ending 30 April 2024

|

Source: Bloomberg, 30 April 2024.

1Note: Equity returns refer to MSCI indices quoted in USD. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

Market view

Markets confront a period of shifting expectations

What a difference a month makes. In the US, instead of the previously projected seven rate cuts in 2024, there is now even a debate over the possibility of the Fed's next move being a rate hike. This has changed the outlook for the US dollar, which remains strong. Asian central banks are under pressure to shore up their currencies and Indonesia’s central bank moved first, surprising the markets with a 25-basis-point rate hike. Ultimately, inflation remains a challenge. Previously, North Asia was expected to benefit from the surge in demand for AI. However, the market is now taking a more cautious approach and it has started to reward value instead of growth. We are currently in a period of changing expectations.

Things might be starting to look up for China

The Chinese government’s plans to address the country’s property market woes sparked a renewed and much-awaited rally in the Chinese equity markets. Even though demand for real estate remains weak in China, the government appears committed to completing the delivery of residential properties that were paid for. Consumer sentiment and confidence are expected to improve as households receive their completed properties. In other positives, Chinese President Xi Jinping’s recent visit to Europe could shore up support for China’s main export markets including green technology, electric vehicles and solar products.

Continue to favour India; ASEAN still attractive within Asia

In India, national elections are underway, and we should see incumbent Prime Minister Modi elected to a third term. On the monetary policy front, the RBI has kept rates flat and India’s currency stable. While pockets of smaller cap stocks are starting to look overly expensive relative to their fundamentals, we do not believe that is the case for the broader index, especially when considering the positive fundamental change and sustainable returns individual companies offer. We continue to favour India and have several new ideas under evaluation.

In ASEAN countries such as Indonesia, economic activity remains relatively robust but inflationary pressures are building. This, however, might be good for Thailand, which is emerging from deflation. The strong dollar is exerting pressure on ASEAN currencies. For the most part, though, the ASEAN region remains an attractive part of Asia. Countries such as Indonesia and the Philippines provide growth opportunities, while Singapore offers a high dividend yield and the potential for structural reform at the state-owned companies, which could unlock shareholder value.

Another consumer tech cycle that is just getting started

The world is fast entering another consumer tech cycle. This time, it is being driven by consumer devices with AI capabilities. This trend is expected to trigger another upgrade cycle as AI-capable devices require newer chipsets. Taiwan and South Korea, being the global centres of tech manufacturing, especially in semiconductors and related fields, stand to benefit from this new cycle. The trajectory is a long one as AI-capable tech transitions from being in high-end devices to mass-market devices. We all await that breakthrough application that will drive the next wave of growth.

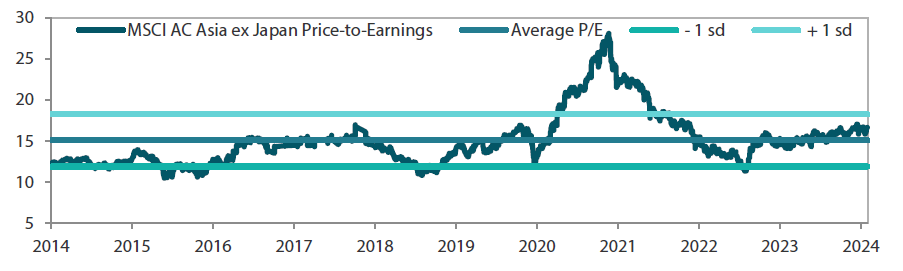

Chart 4: MSCI AC Asia ex Japan price-to-earnings

Source: Bloomberg, 30 April 2024. Ratios are computed in USD. The horizontal lines represent the average (the middle line) and one standard deviation on either side of this average for the period shown. Past performance is not necessarily indicative of future performance.

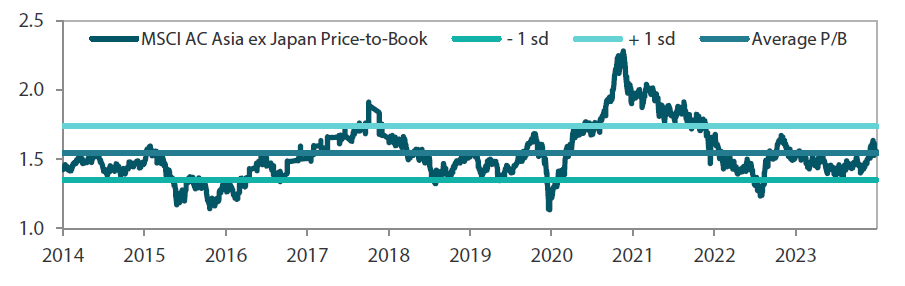

Chart 5: MSCI AC Asia ex Japan price-to-book

Source: Bloomberg, 30 April 2024. Ratios are computed in USD. The horizontal lines represent the average (the middle line) and one standard deviation on either side of this average for the period shown. Past performance is not necessarily indicative of future performance.