Exhibiting an extensive track record of outperformance versus big caps and offering good diversification from traditional equities, we believe that Asian small-cap stocks provide numerous investment merits for long-term investors.

Asian small caps make a strong comeback

Asian small capitalisation (cap) stocks, which were largely overlooked by the markets from 2016 to 2019, have started to capture the attention of investors of late, owing to the strong gains they have racked up since March 2020 when global equity markets hit a bottom at the onset of the COVID-19 pandemic.

Over the 12 months ended 31 March 2021, regional small caps, as measured by the MSCI AC Asia ex Japan Small Cap Index, returned more than 80% in US dollar (USD) terms, outperforming their large- and mid-caps peers (as measured by the MSCI AC Asia ex Japan Index), which generated USD gains in excess of 50%.

With the regional economic recovery currently in full swing, boosted by vaccine-led optimism, ample liquidity in the global financial systems and a pick-up in corporate earnings, Asian small caps—currently in the early stage of a sustainable rebound—should maintain their upward momentum in the foreseeable future, in our view.

On top of the favourable short-term outlook, Asian small-cap stocks’ longer-term prospect also looks promising. As we see it, the investment case for Asia’s smaller and lesser-known listed companies with an undersized market cap currently looks strong. We explain in detail the traits, opportunities and appeal of Asian small caps and the benefits of investing in this unique equity asset class.

Nimble and fast growing

Nimble, fast growing and at an early stage of development, small-cap companies have the ability to seize market opportunities at a quick pace and generate exceptional earnings growth. To be sure, innovative smaller companies with robust business models and scalable strategies could grow exponentially, particularly if their niche products or services are successful. The essence of small-cap investing is finding the big winners of tomorrow.

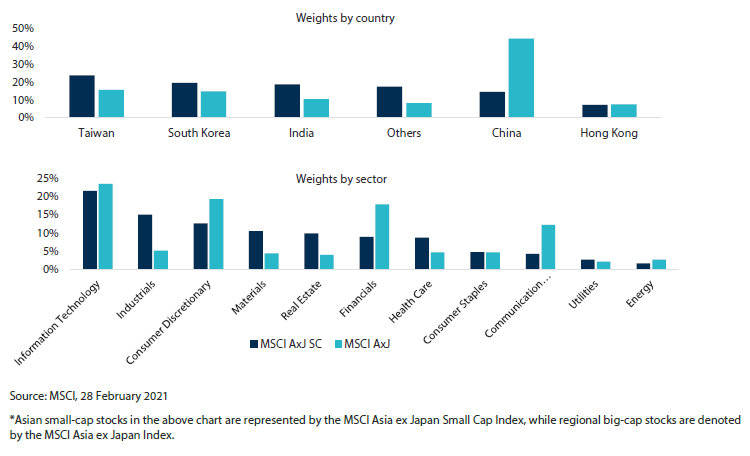

Small and large caps have different country and sector weights

Asian large caps have a larger weight in China versus regional small caps. The large caps of Asia also have higher percentage of weights in sectors, namely financials and consumer discretionary, relative to small caps, which have more exposure in industrials, materials, real estate and healthcare (see Chart 1). As such, investing in small caps do allow for greater diversification from other traditional equity strategies, which tend to be large-cap centric.

Chart 1: Country and sector weights of Asia small caps* and large caps*

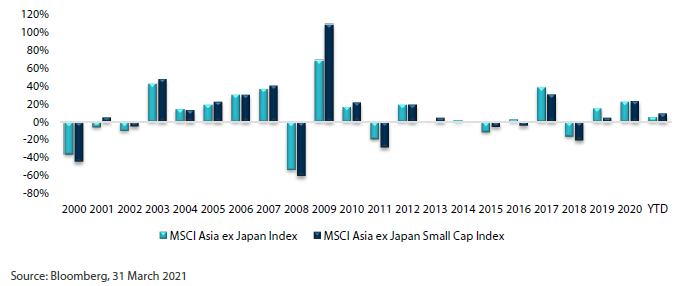

A long track record of outperformance

Over the past two decades, Asian small caps (as measured by the MSCI Asia ex Japan Small Cap Index) have outperformed their bigger-cap counterparts (as measured by the MSCI Asia ex Japan Index) 64% of the time. In addition, regional small caps have significantly outpaced Asian large caps during distinct periods, especially phases of recovery after a major market selloff, such as in 2001, 2009 and the first quarter of 2021 (see Chart 2).

The 20-year track record of outperformance of Asian small cap versus large caps certainly gives comfort to long-term investors that having some exposure to stocks of regional smaller companies could enhance the overall returns of their equity portfolios over the long run.

Chart 2: Asian small caps* outperformed regional big caps* 64% of the time in the past 20 years

*Asian small-cap stocks in the above chart are represented by the MSCI Asia ex Japan Small Cap Index, while regional big-cap stocks are denoted by the MSCI Asia ex Japan Index, all of which are quoted in US dollars. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

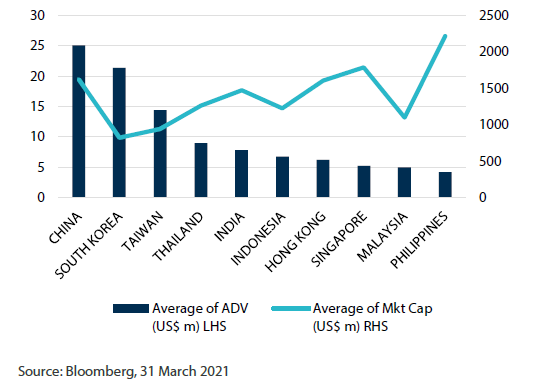

Regional small caps have ample liquidity

Small caps tend to have thinner trading volumes as compared with their big-cap counterparts; but that doesn’t imply that all Asian small caps are illiquid. Small-cap stocks that are listed in the North Asian markets, such as China, South Korea and Taiwan, generally have ample liquidity, as measured by the average daily value (ADV) of trades (see the Chart 3). For instance, the ADV of equity trades in China averages USD 25 million a day, while that of South Korea exceeds USD 20 million each day.

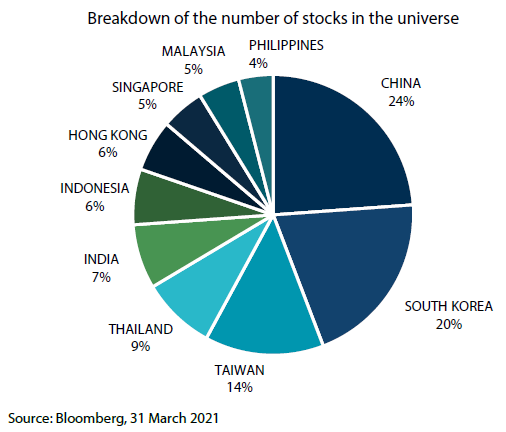

Another key point pertaining to liquidity is that the bulk of stocks in the Asian small-cap universe comes from China, South Korea and Taiwan—three of the most liquid Asian equity markets for small caps. The fact that the liquid markets of North Asia is home to more than half of all Asian small-cap stocks in the universe (see Chart 4) debunks the myth that most regional small caps are illiquid.

Chart 3: Small-cap ADV by country

Data set is based on our small-cap investable universe: USD 200 million to USD 5 billion in terms of market cap, 3-month ADV > USD 1 million

Chart 4: Percentage of stocks per market in the Asian small-cap universe

Data set is based on our small-cap investable universe: USD 200 million to USD 5 billion in terms of market cap, 3-month ADV > USD 1 million

Access to a larger opportunity set

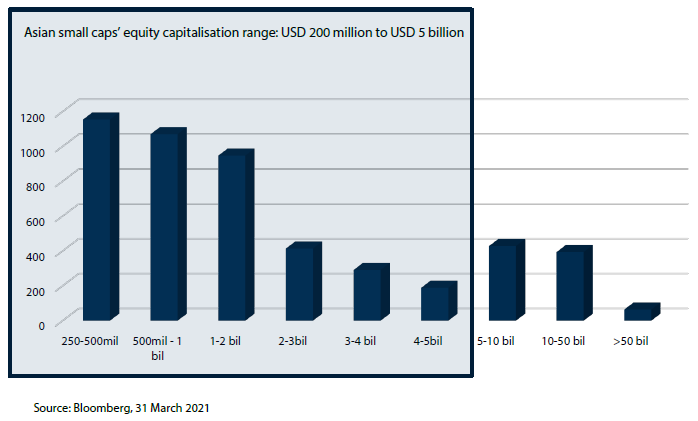

The large number of Asian small-cap companies, many of which are relatively unknown to investors, represents potentially overlooked opportunities. At the outset, there are over 2,000 regional small-cap stocks with a market cap of less than USD 1 billion and more than 1,000 counters with a market cap of between USD 1-3 billion to choose from versus a universe of less than 500 big-cap stocks with a market cap of between USD 5-10 billion (see Chart 5).

Chart 5: Number of companies by market-cap band (USD)

Data set is based on our small-cap investable universe: USD 200 million to USD 5 billion in terms of market cap, 3-month ADV > USD 1 million

Likewise, there are more small-cap benchmark stocks in the region than benchmark stocks in the big- and mid-cap category. To illustrate, there are more than 1,400 stocks in the MSCI Asia ex-Japan small-cap universe as compared with 1,182 stocks (as at 31 March 2021) that are constituents of the MSCI Asia ex Japan Index, which captures large- and mid-cap representation in the Asia ex-Japan equity markets.

All things considered, the large opportunity set in the Asian small-cap universe offers active investors a wider scope to select stocks from the bottom up and sniff out the potential small-cap winners and avoid the losers.

Lack of coverage of small caps gives opportunities to capture alpha and unearth gems

Investing in Asian small caps truly encapsulates the essence of active equity investing, in which stock selection adds value and drives alpha in this under-researched equity space (alpha is generally defined as returns in excess of a benchmark’s performance). We believe that there is a lot of price inefficiency in the Asian small-cap market, where stock prices do not accurately reflect their true value.

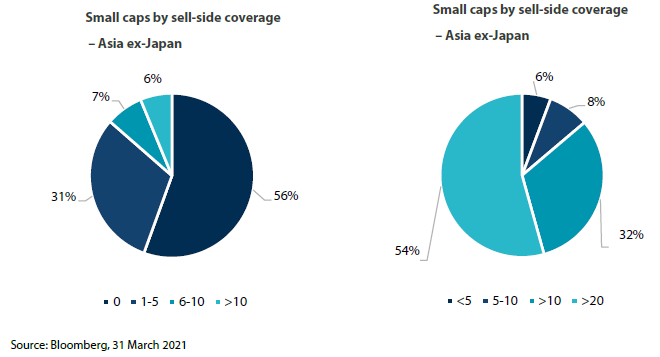

Indeed, more than half of all Asian small-cap stocks in the investable universe are not covered by any sell-side equity analysts (or analysts from brokerages) and only 31% of them have coverage from sell-side analysts numbering one to five (see Chart 6). In contrast, a typical Asian large-cap stock is covered by at least 10 sell-side analysts.

In our view, the limited sell-side coverage of regional small caps offers opportunities for active investors to capture alpha and unearth “hidden gems” due to the mispricing in the Asian small-cap equity market, where there is a large information gap to exploit.

Chart 6: Small- and large-caps’ sell-side coverage (denoted by the number of analysts)

Data set is based on our small-cap investable universe: USD 200 million to USD 5 billion in terms of market cap, 3-month ADV > USD 1 million. Large caps are defined as those with a market cap of more than USD 5 billion.

Backed by strong and committed shareholder base

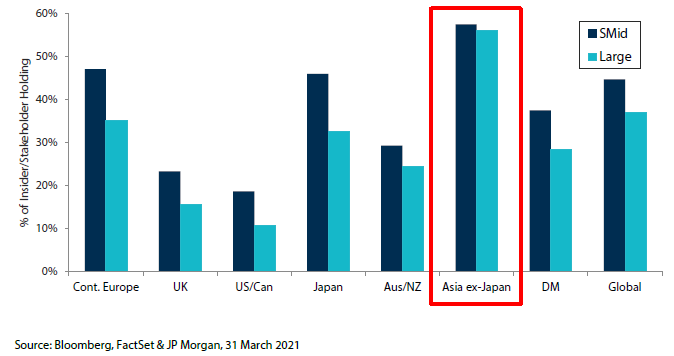

Small- and mid-cap companies generally have higher family and management ownership (see Chart 7), representing more “skin in the game” or higher vested interest of the owners, which share an aligned goal towards success with minority shareholders. Family and management ownership, akin to higher insider ownership, are stakeholders who tend to be more committed to their owned companies than hired CEOs, managers and executives, all of whom have relatively less “skin the in game”.

Chart 7: Insider stakes of small- and mid-caps vs large caps

Having a strong, committed and entrepreneurial management team could be the driving factor of success for many of the smaller companies, which tend to be more financially constrained and more vulnerable to product failures, dramatic slowdown in sales or a surge in the cost of capital as compared to bigger companies.

Summary

We see a strong investment case for Asian small caps, which have different country and sector weights relative to their bigger-cap peers; a long track record of outperformance; and ample level of liquidity. The large number of small caps in the region and their under-research nature also give investors a wider scope to select stocks from the bottom up and sniff out hidden gems and capture excess returns.

Nimble, fast growing and at an early stage of development, small-cap companies have the ability to seize market opportunities at a quick pace, generate exceptional earnings growth and grow capital faster than their big-cap counterparts. That’s why investing in Asian small-cap stocks remains a potentially lucrative proposition for long-term investors, in our view.