Summary

- The US Treasury (UST) yield curve flattened in November. Risk markets rallied after the US presidential election. Investor confidence was lifted following positive trial results of a COVID-19 vaccine. Yields subsequently retracted part of their earlier rise on news of soaring COVID-19 infection rates in the US and Europe and near-term downside risks to the economy. Overall, the benchmark 2-year and 10-year yields ended about 0.6 basis points (bps) and 3.4 bps lower, to 0.149% and 0.841%, respectively.

- Asian credits returned 1.27% in November, mainly due to credit spreads tightening by about 22.4 bps on the back of improved risk sentiment. High-grade (HG) credits gained 0.95%, as spreads narrowed 14.3 bps, while high-yield (HY) credits returned +2.36%, with spreads tightening about 55.3 bps. Primary market activity was relatively muted in November, particularly within the HG space, as companies had largely front-loaded issuance ahead of the US presidential election.

- Within the region, inflationary pressures remained mostly muted. Regional growth registered a meaningful bounce in the third quarter (3Q20) as governments eased COVID-19 containment measures, while monetary authorities in Indonesia and the Philippines lowered their respective policy rates.

- Overall, we expect Indonesian bonds to outperform. Slow growth, further monetary policy easing and increasing Emerging Market (EM) inflows, in our view, should support the continued outperformance of Indonesian bonds. On currencies, we are positive on the Chinese yuan (CNY), South Korean won (KRW), Singapore dollar (SGD) and Indonesian rupiah (IDR).

- We expect Asian credit spreads to continue tightening slowly over the medium-term, although downside risks remain. Broad risk sentiment and direction of credit spreads for the remainder of the year are likely to be determined by events and developments in December.

Asian rates and FX

Market review

The UST yield curve flattens in November

Risk markets rallied after the US presidential election, as investors were relieved to see the event pass without major surprises. In addition, strong economic data from major Asian economies reinforced signals of a broadening economic recovery. As greater clarity on the US elections outcome emerged, long-end UST yields moved lower on tempered expectations of fiscal stimulus. Investor confidence was meaningfully lifted following the announcement of positive trial results of a COVID-19 vaccine. Yields subsequently retracted part of their earlier rise on news of soaring COVID-19 infection rates in the US and Europe and near-term downside risks to the economy. The announcement that the US Treasury will end the Federal Reserve's (Fed) emergency lending facilities by year-end stirred some uncertainty in markets. Towards month-end, risk tone turned positive anew following pronouncements that the formal transition to US President-elect Joe Biden can commence. Reports around cabinet picks for the Biden administration, particularly the choice of former Fed Chairperson Janet Yellen as head of US Treasury, were received positively by markets. Overall, the benchmark 2-year and 10-year yields ended about 0.6 bps and 3.4 bps lower, to 0.149% and 0.841%, respectively.

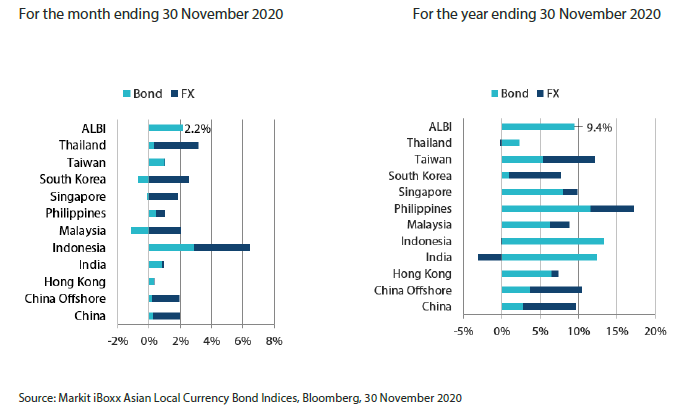

Chart 1: Markit iBoxx Asian Local Bond Index (ALBI)

Note: Bond returns refer to ALBI indices quoted in local currencies while FX refers to local currency movement against USD. ALBI regional index is in USD unhedged terms. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

Inflationary pressures remain mostly muted in the region

Headline consumer price index (CPI) prints rose in India, the Philippines and Thailand, were largely unchanged in Indonesia and moderated in China, South Korea, Malaysia and Singapore. Headline inflation in India hit 7.6% in October, accelerating from 7.3%, on the back of a spike in food inflation. Similarly, the slight acceleration in the Philippines' annual inflation rate was prompted partly by higher food prices. Meanwhile, Malaysia's headline CPI moderated in October, contracting for the eighth consecutive month. Deflationary pressures deepened partly due to a moderation in transportation and communication inflation. In China, the CPI dropped to 0.5% year-on-year (YoY) on the back of plunging pork price inflation. Elsewhere, inflation in Singapore dipped to -0.2% in the same month, as private transport costs declined and accommodation inflation eased.

Real gross domestic product (GDP) growth rebounds in the third quarter

Following steep contractions in the second quarter, regional growth registered a meaningful bounce in the July to September period as governments eased COVID-19 containment measures. The economic re-opening in Thailand prompted a rise in government spending, which supported the significant improvement in Thailand's GDP growth over the same period. Growth in Indonesia also showed signs of recovery, its contraction slowing to -3.5% in the third quarter after declining -5.3% in the previous quarter, as faster budget execution prompted an expansion in government spending. In India, third quarter growth registered -7.5% YoY, a sharp rebound from the 23.9% decline in the prior quarter. The recovery was uneven, led mainly by fixed investment, while there was a notable reduction in government spending. Elsewhere, the Philippine economy shrank 11.5% YoY (from -16.9%) in the third quarter. The slower recovery was owed largely to weak public sector spending.

Monetary authorities in Indonesia and the Philippines lower their respective policy rates

Both the BI and Bangko Sentral ng Pilipinas (BSP) delivered a 25 bps rate cut in November. BI's move came after the central bank kept rates unchanged for three consecutive meetings. According to BI, there was a need to "expedite" the economic recovery. Meanwhile, BSP trimmed interest rates after standing pat at its previous two meetings. Notably, the policy statement highlighted growth concerns, which suggests that the bank is leaving the door open for further easing.

India announces fresh stimulus measures; Thailand moves to reign in the baht; Malaysia passes measures to allow increased Employees Provident Fund (EPF) withdrawals

Malaysia's parliament passed the 2021 federal budget, which was largely seen as a confidence vote in Prime Minister Muhyiddin Yassin's government. That said, the budget included measures that allowed increased EPF withdrawals for select members, as well as the reduction from 11% to 9% in the minimum statutory rate of EPF contribution for employees, which prompted some concern about future demand for Malaysian bonds. Meanwhile, the Indian government announced fresh policy measures intended to primarily help stressed sectors and generate employment. The fiscal cost of the measures announced amounts to around Indian rupee (INR) 2.6 trillion. Elsewhere, Thailand moved to cool rapid gains in the Thai baht. Apart from increasing the scrutiny of fund flows into bonds, the Bank of Thailand also moved forward measures that were initially intended to be implemented early next year, to encourage capital outflows.

Market outlook

Positive on Indonesian bonds

We anticipate the combination of growth recovery supported by vaccine availability and still dovish Fed to support the overall positive risk tone in markets. This should also prompt increased flows into EM including Asia. We expect Indonesian bonds to outperform on an intra-Asia basis as markets favour local currency debt that offers higher carry. With FX stability ostensibly achieved, BI has resumed easing of monetary policy. We also expect further rate cuts by the central bank as focus has clearly shifted to supporting growth. Slow growth, further monetary policy easing and increasing EM inflows, in our view, should support the continued outperformance of Indonesian bonds.

Positive on CNY, KRW, SGD and IDR

We expect Asian currencies to appreciate against the US dollar (USD), with the CNY, KRW and SGD—being relatively more trade-sensitive—outperforming. The IDR would also benefit from increased foreign flows, whereas lingering political risk will be key headwinds for the Malaysian ringgit and Thai baht, which may cause them to lag their peers.

Asian credits

Market review

Asian credits rally in November as positive vaccine developments lift sentiment

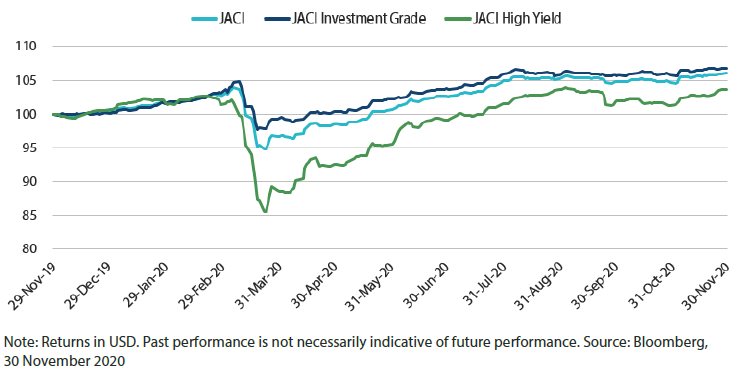

Asian credits returned 1.27% in November, mainly due to credit spreads tightening by about 22.4 bps on the back of improved risk sentiment. HG credits gained 0.95%, as spreads narrowed 14.3 bps, while HY credits returned +2.36%, with spreads tightening about 55.3 bps.

Asian credits staged a strong rally after the US presidential election as investors were relieved to see the event pass without major surprises. In addition, strong economic data from major Asian economies reinforced signals of a broadening economic recovery. Spreads continued to tighten as greater clarity on the US presidential election outcome emerged. Investor confidence was significantly lifted following the announcement of positive trial results for a COVID-19 vaccine. This largely overshadowed news of soaring COVID-19 infection rates in the US and Europe. The US-China tensions were in focus again mid-month, after US President Donald Trump signed an executive order banning investments in Chinese firms deemed to be owned or controlled by the Chinese military. At the same time, concerns about a possible slowdown in the US economic recovery rose. These factors, together with news that the US Treasury will end the Fed’s emergency lending facilities by year-end, stirred some uncertainty in markets and pushed spreads modestly wider. However, the slight retracement in spreads was very brief, as risk tone turned positive anew following pronouncements that the formal transition to President-elect Biden can commence. Reports around cabinet picks for the Biden administration, particularly the choice of former Fed Chairperson Yellen as head of US Treasury, were received positively by markets. Demand technicals for Asian credits were particularly strong in November. The reduced political uncertainty and vaccine hope supported robust inflows into EM hard currency bond funds.

Improved market sentiment prompted spreads of all major country segments to end tighter. India led the spread tightening, while China underperformed. Sentiment towards Chinese credits was negatively affected by the renewed escalation in US-China tensions and recent high-profile defaults of several Chinese state-owned enterprises.

Primary market activity moderates

Primary market activity was relatively muted in November, particularly within the HG space, as companies had largely front-loaded issuances ahead of the US presidential election. There were 49 new issues amounting to USD 16.73 billion. Within the HG space, 22 new issues amounting to USD 8.25 billion were raised. Meanwhile, the HY space saw USD 8.48 billion being raised from 27 new issues, including the USD 2.8 billion Additional Tier 1 instrument from Bank of Communications.

Chart 2: JP Morgan Asia Credit Index (JACI)

Market outlook

Asian credit spreads to continue tightening slowly on signs of fundamental recovery though downside risks remain

Asian credit spreads are expected to continue tightening slowly over the medium-term. Most Asian economies have contended with COVID-19 relatively well and this has helped their economies recover, with high-frequency indicators suggesting a recovery is underway. This also ties in with signs of improvement in corporate credit fundamentals. Credit-supportive fiscal and monetary policies are also expected to remain in place in most developed and EM countries, even if incremental easing measures are likely to moderate going forward. Progress on vaccines development and better treatment for COVID-19 cases further reinforce the positive backdrop.

Nevertheless, given the sharp rally in credit spreads over recent months, the pace of tightening should slow with more regular episodes of market pull-backs. Broad risk sentiment and direction of credit spreads for the remainder of the year are likely to be determined by events and developments in December, with uncertainties relating to the outcomes of these events having intensified—an executive order banning US investments in military-affiliated China corporates being the latest notable example. The order should not dent fundamentals too much but could lead to some technical pressure, which remains a risk under the incoming US administration. Therefore, some volatility is expected as the market waits for further clarification on the executive order. In addition, there are still considerable challenges in vaccine production, delivery and administration. Therefore, vaccine-related issues could still add to the near-term uncertainties.